Old vs. New Tax Regime: Which One Actually Saves You More Tax?

Budget 2025 made income up to ₹12 lakh completely tax-free, but does that automatically make the new regime the right choice for you? Here's a simple breakdown of tax slabs, deductions, and a real salary example to help you decide before you file.

By Khusbu Modi on May 04, 2026

Old vs. New Tax Regime: Which Should You Choose for FY 2025-26

(Tax Year 25-26)?

If you earn income in India, you face one important choice every year: the old tax regime or the new one? From April 2025, this decision carries more weight than ever. Budget 2025 has made the new regime significantly more attractive for most salaried earners, but the old regime still holds its ground for taxpayers who plan their deductions well. Here is what you need to know to make the right call.

What Changed from Budget 2025?

The Union Budget 2025 introduced two changes that fundamentally shift this decision:

- Rebate under Section 87A increased to ₹60,000 under the new regime, making normal taxable income up to ₹12 lakh completely tax-free.

- Standard deduction raised to ₹75,000 for salaried employees and pensioners under the new regime (up from ₹50,000).

The combined impact: a salaried individual with a gross salary of up to ₹12.75 lakh pays zero income tax under the new regime - no investment required, no paperwork and no declarations.

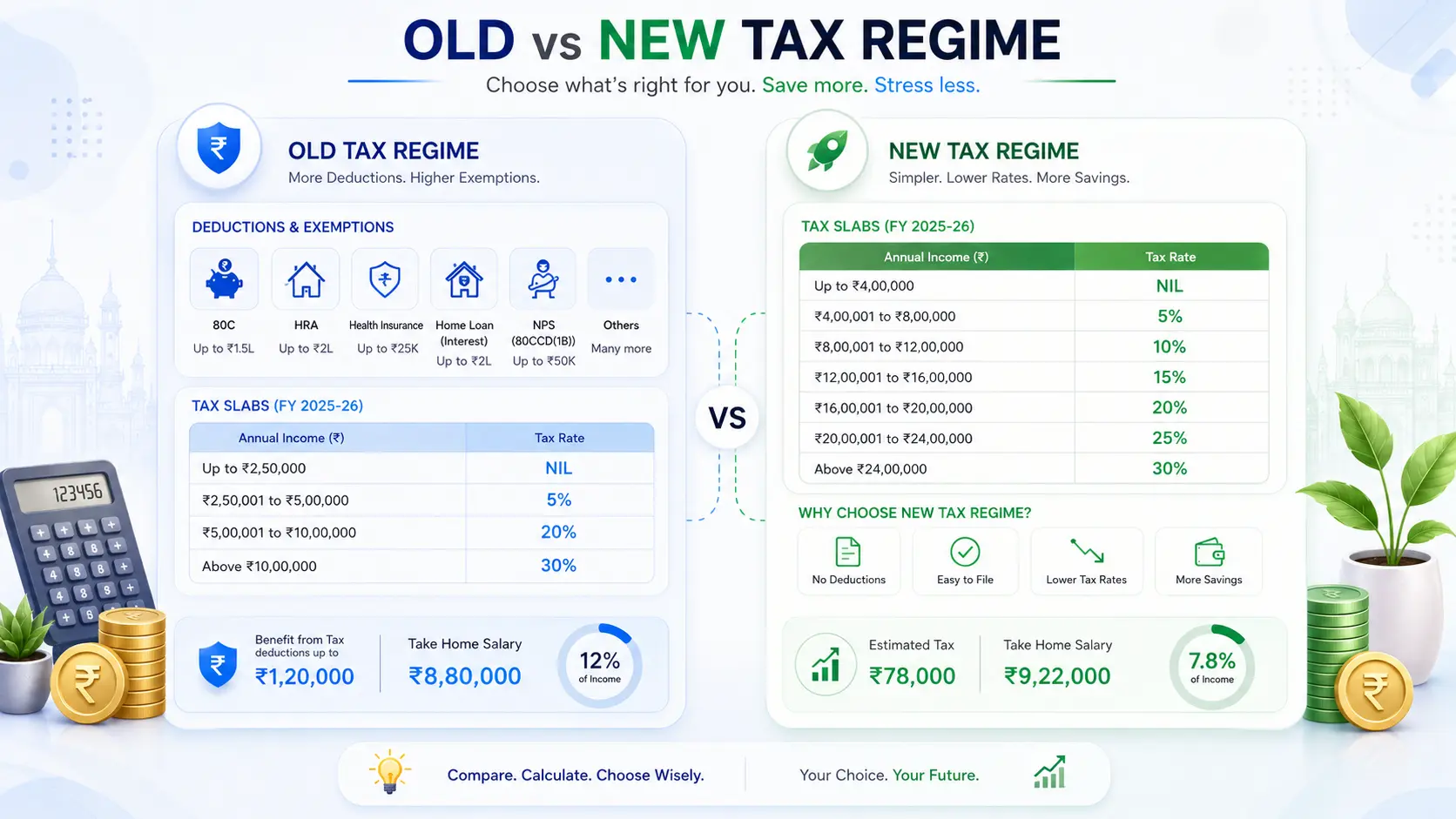

New Tax Regime: Lower Rates, Fewer Deductions

Tax Slabs for FY 2026-27 (now Tax Year 2026-27):

|

Income Range |

Tax Rate |

|

₹0 – ₹4 lakh |

0% |

|

₹4 – ₹8 lakh |

5% |

|

₹8 – ₹12 lakh |

10% |

|

₹12 – ₹16 lakh |

15% |

|

₹16 – ₹20 lakh |

20% |

|

₹20 – ₹24 lakh |

25% |

|

Above ₹24 lakh |

30% |

Which deductions not available under the new regime, some common examples:

- Section 80C - Deductions up to ₹1.5 lakh on investments such as PPF, ELSS mutual funds, life insurance premiums, NSC, 5-year fixed deposits, home loan principal repayment and children's tuition fees.

- Section 80D - Premium paid on health insurance policies: up to ₹25,000 for self and family; up to ₹50,000 if your parents are senior citizens.

- Section 24(b) - Home loan interest deduction up to ₹2 lakh per year on self-occupied property.

- HRA Exemption - Exemption on House Rent Allowance based on actual rent paid, city of residence, and salary.

- Section 80E - Interest on education loans for higher studies, with no upper limit, available for up to 8 years.

- LTA (Leave Travel Allowance) - Exemption on travel costs for domestic travel taken with family, claimable twice in a block of four years.

What you can still claim:

- Section 80CCD(2) — Employer's contribution to the National Pension System (NPS), up to 14% of basic salary plus DA. This is one of the most valuable deductions still accessible under the new regime and is often underutilised.

Who it suits:

Salaried employees in the early stages of their career, individuals with limited investments, or anyone whose total eligible deductions fall below the break-even threshold for their income level.

Old Tax Regime: Higher Rates, Full Deductions

Tax Slabs for FY 2026-27 (now Tax Year 2026-27):

(for individuals upto 60 years of age)

|

Income Range |

Tax Rate |

|

₹0 – ₹2.5 lakh |

0% |

|

₹2.5 – ₹5 lakh |

5% |

|

₹5 – ₹10 lakh |

20% |

|

Above ₹10 lakh |

30% |

The old regime's slab rates are higher, but it unlocks a wide range of deductions that can significantly reduce your taxable income.

Key deductions available:

- Section 80C - Up to ₹1.5 lakh on PPF, ELSS, life insurance premiums, home loan principal, NSC, ULIP, and children's tuition fees.

- Section 80D - Health insurance premiums up to ₹25,000 for self and family; up to ₹50,000 if your parents are senior citizens. Maximum combined deduction: ₹75,000.

- Section 24(b) - Home loan interest on self-occupied property up to ₹2 lakh per financial year.

- HRA Exemption - Calculated as the lowest of: actual HRA received, 50% of basic salary (metro cities) or 40% (non-metro), or actual rent paid minus 10% of basic salary.

- Section 80E - Full interest paid on education loans for higher studies, deductible for up to 8 consecutive years from the year repayment begins.

- LTA - Actual travel expenses for domestic trips with immediate family, claimable for two journeys in a four-year block.

- Section 80CCD(1B) - Additional ₹50,000 deduction on your own NPS contributions, over and above the ₹1.5 lakh Section 80C limit.

- Standard deduction: ₹50,000

- Section 87A rebate: ₹12,500 for taxable income up to ₹5 lakh

Who it suits:

Individuals with home loans, those paying significant rent and claiming HRA, people with active 80C portfolios and health insurance, and self-employed professionals with multiple eligible deductions.

Real-World Comparison: ₹15 Lakh Salary

Scenario 1- Modest deductions (HRA deduction ₹2L + Section 80C ₹1.5L + standard deduction):

|

Components |

New Regime |

Old Regime |

|

Gross Income |

₹15,00,000 |

₹15,00,000 |

|

Less: Standard Deduction |

₹75,000 |

₹50,000 |

|

Less: HRA deduction |

Not allowed |

₹2,00,000 |

|

Less: Section 80C |

Not allowed |

₹1,50,000 |

|

Taxable Income |

₹14,25,000 |

₹11,00,000 |

|

Tax (before cess) |

₹93,750 |

₹1,42,500 |

|

Add: 4% Cess |

₹3,750 |

₹5,700 |

|

Net Tax Payable |

₹97,500 |

₹1,48,200 |

Result: New regime saves ₹50,700.

Scenario 2 - Heavy deductions (HRA ₹3L + Section 80C ₹1.5L + Home Loan Interest u/s 24b ₹2L + standard deduction):

|

Components |

New Regime |

Old Regime |

|

Gross Income |

₹15,00,000 |

₹15,00,000 |

|

Total Deductions |

₹75,000 |

₹7,00,000 |

|

Taxable Income |

₹14,25,000 |

₹8,00,000 |

|

Tax (before cess) |

₹93,750 |

₹72,500 |

|

Add: 4% Cess |

₹3,750 |

₹2,900 |

|

Net Tax Payable |

₹97,500 |

₹75,400 |

Result: Old regime saves ₹32,500.

The takeaway is clear: it is not the income level alone that determines which regime wins - it is the size and legitimacy of your deductions. For the same ₹15 lakh salary, the winning regime changes entirely depending on what you can claim.

How to Switch Between Regimes

The new regime is the default from Tax Year 2025-26. To opt for the old regime:

- If you are salaried: Select "No" to Section 115BAC when filing your ITR. Inform your employer at the start of the financial year so TDS is deducted correctly. You can change your regime choice every year.

- If you are self-employed or have business income: File Form 10-IEA along with your ITR to opt for the old regime. Note that once you opt out of the new regime, switching back is not straightforward, choose carefully.

The Bottom Line

The new regime is the smarter default for most salaried individuals, particularly those earning up to ₹12.75 lakh or those without significant deductions. For those with a home loan, HRA claims, and an active 80C portfolio, the old regime can still deliver meaningful savings, but only if your total eligible deductions cross the break-even threshold for your income level.

Before you finalise your choice, add up every deduction you genuinely qualify for — Section 80C investments you were already planning to make, your actual health insurance premiums under Section 80D, home loan interest under Section 24(b), and your HRA exemption. Compare the net tax under both regimes. That calculation, not assumptions, should drive your decision.

Disclaimer: This article is for informational purposes only and does not constitute tax advice. Consult a qualified Chartered Accountant before making your regime selection.